A defined contribution scheme is a pension scheme for employees. The contribution paid by the employer forms the basis for the pension capital. A pension is bought from this on the retirement date. In a defined contribution scheme, the amount and type of pension are not fixed in advance.

The defined contribution is invested up to the retirement date. On the retirement date a pension is purchased from the available assets. The employee runs a risk with the investments, but also benefits when high returns are achieved.

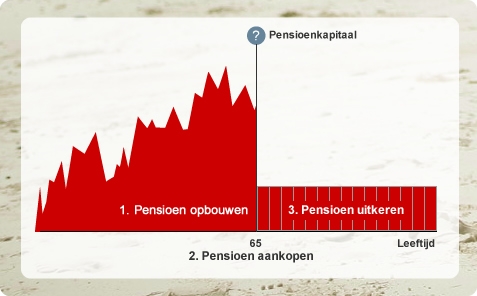

How does a defined contribution scheme work?

-

Accruing a pension

As the employer, you determine the pension contribution to spend on the pension of your employees. The defined contribution depends on the salary and age of the employees. This contribution is fixed in advance. So, as an employer, you know exactly what to expect.Because we are investing, the pension capital is not guaranteed. How much pension capital there will be for your employees depends on the results of the investments.

-

Purchasing a pension

On the retirement date, the accrued pension capital is paid out. Your employees may use it only to purchase a periodic pension benefit. It is up to them to decide from which insurer they want to buy. The amount and type of pension (and the benefits) are not yet fixed. These depend, for example, on the interest rate at the time the pension is purchased.

-

Paying out a pension

As soon as your employee has selected a provider to pay out his pension, his accrued pension capital will be converted into a lifelong monthly pension benefit.

Zwitserleven defined contribution schemes with investments

- The Nu Pensioen (Pension Now) is clear, responsible and complete. A new and clear way to accrue an investment-based pension. This pension scheme is a product of Zwitserleven IORP and Zwitserleven.

- The Exclusive Pension offers the most options. For Exclusive Pension, the pension contributions are invested either by Zwitserleven or by your employees. Zwitserleven provides full transparency on costs.

Waarom kiezen voor beschikbare premieregeling? Why choose a defined contribution scheme?

The employer determines the amount of the contribution and will not be faced with any surprises. In a defined contribution scheme, employees can sometimes choose what happens with the defined contributions. Read more about all the pros and cons of a defined contribution scheme for you and your employees in the brochure of the Dutch Association of Insurers.

Zwitserleven defined contribution scheme pension product

- For Exclusief Pensioen (Exclusive Pension) the pension contributions are invested either by Zwitserleven or by your employees. Zwitserleven provides full transparency on costs.

Customised defined contribution scheme pension

A defined contribution scheme is one of the options in a customised solution for larger employers. Zwitserleven will be happy to discuss the details of your pension scheme with you.

Need a quote or advice?

As a good employer, you want to choose a pension that is right for your business and for your employees. We have a wide range of options to suit every type of business. Such as an investment-based defined contribution pension scheme, possibly in conjunction with Nettopensioen. A complete overview of our products is available.

If you would like to know more about this or any of our other pension schemes, or would like to get specific advice on a pension scheme for your employees, contact an independent financial adviser. Zwitserleven has an excellent relationship with a large number of professional insurance advisers.